Quick Answer: Michigan employers with 50 or more employees and stable workforces can save 15 to 20% on healthcare costs by moving to a self-funded or level-funded health plan. The decision depends on cash flow, workforce stability, and risk tolerance, not size alone. This guide walks Michigan CFOs and business owners through the evaluation framework, regulatory considerations, and implementation timeline for 2026.

Table of Contents

-

- Why are Michigan employer healthcare costs rising so fast?

- How do self-funded, level-funded, and fully insured plans compare?

- Is my company ready to self-fund? A Readiness Assessment Framework

- What does Michigan’s regulatory environment mean for self-funded plans?

- What does the implementation timeline look like?

- What to Expect in Year One

- What should Michigan employers do next?

- Frequently Asked Questions About Self-Funded Health Plans in Michigan

- About the Author, Mike Hill

- Sources

Why are Michigan employer healthcare costs rising so fast?

If you’re reading this, you probably already know: your health insurance renewal wasn’t pretty this year. With over 25 years in the employee benefits industry, our team can tell you the 2025–2026 renewal cycle has been the most contentious we’ve ever seen. But the actual numbers tell the story better than any anecdote.

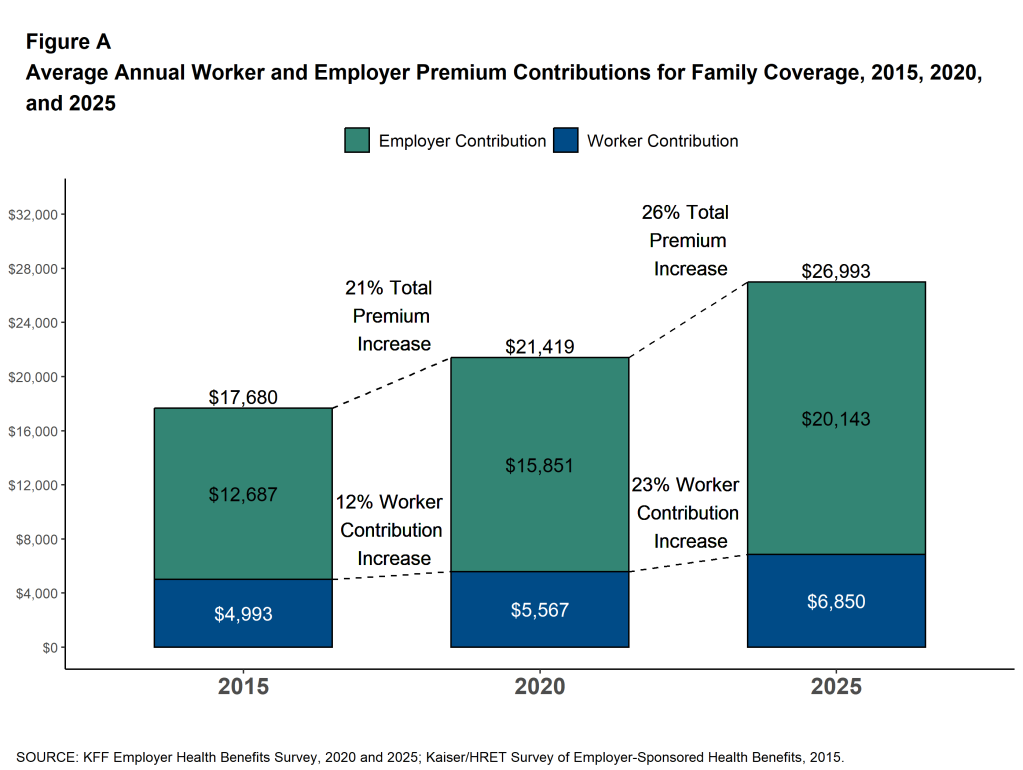

Starting with national data, Mercer’s 2025 National Survey of Employer-Sponsored Health Plans shared that the average total cost of employer-sponsored health insurance was $17,496 per employee in 2025, a 6.0% increase. Mercer projects that the figure will exceed $18,500 per employee in 2026. That 6.7% projected jump marks the highest growth rate in 15 years, and before employers make plan design changes, the raw cost increase runs closer to 9%. The 2025 KFF Employer Health Benefits Survey confirms the trend. Average annual premiums reached $9,325 for single coverage and $26,993 for family coverage, up 5% and 6%, respectively.

The structural reason isn’t hard to find. Michigan ranks as the 4th least competitive commercial health insurance market in the country, according to the American Medical Association’s 2024 competition analysis. Michigan’s market is dominated at the state level by BCBSM, which holds commanding share across virtually every region. When competition is limited, employers have little leverage, and carriers have little incentive to hold costs down.

Michigan is no longer below the national average. For years, Michigan’s employer-sponsored premiums ran below U.S. averages, in part because BCBSM’s dominant market position kept administrative costs relatively contained within a highly consolidated system. But consolidation is a double-edged sword: the same concentration that once produced pricing stability now produces pricing power. According to a December 2025 report by SHADAC (the State Health Access Data Assistance Center, a nonpartisan health policy research center at the University of Minnesota), Michigan’s average employer-sponsored premiums have reached $8,885 for single coverage and $24,252 for family coverage. Researcher Andrea Stewart noted that Michigan now experiences increases “on par with the U.S. level.” SHADAC also flagged Michigan as one of only six states where single-coverage deductibles rose significantly from 2023 to 2024.

What’s Driving Cost Increases in Michigan Specifically?

Michigan’s Department of Insurance and Financial Services (DIFS) approved an average 11.1% rate increase for the small group market in 2026. The individual market saw an even steeper increase, with DIFS approving a 20.2% increase for 2026, up from 10.9% in 2025. Blue Cross Blue Shield of Michigan received an 11.2% increase, Blue Care Network 12.4%, and Priority Health 9.8%. For context, BCBSM reported a $1.7 billion underwriting loss in 2024, paying $1.04 in claims for every premium dollar collected (Crain’s Detroit Business).

Every major consulting firm projects an 8.5-9.5% gross medical cost trend for 2026. PwC’s Health Research Institute projects 8.5%. Aon projects 9.5%. Segal forecasts 9% for medical and 11% for prescription drugs. The Business Group on Health (covering 11.6 million lives) projects a 9% median gross increase. Those increases are driven by GLP-1 medications, specialty drugs, provider consolidation, rising cancer treatment costs, and record mental health utilization.

There are also Michigan-specific concerns that need more attention. Three hospital systems (Corewell Health, Henry Ford Health, and Michigan Medicine) now control 64% of hospital market share. That’s double the 30% they held in 2019, according to BCBSM CEO Tricia Keith.

The insurance market tells a similar story: BCBSM dominates commercial coverage statewide, and Priority Health, Michigan’s second-largest insurer, is owned by Corewell Health, putting the state’s largest hospital system and its second-largest insurer under the same roof.

Hospital prices in Michigan have risen more than 250% since 2000, tripling the rate of general inflation. The UnitedHealthcare/Corewell Health contract dispute, which removed four Southeast Michigan hospitals from the UHC network for UHC plans in January 2026, is a direct symptom of this consolidation.

These increases are not a one-year blip. They’re structural, and they are why more Michigan employers than ever are exploring self-funded alternatives.

How do self-funded, level-funded, and fully insured plans compare?

Not all health plan funding strategies deliver equal results. Here’s a side-by-side comparison of the three main approaches, tailored to what Michigan mid-market employers (50 to 500 employees) care about most.

| Consideration | Fully Insured | Level-Funded | Self-Funded |

|---|---|---|---|

| Who bears the risk? | Insurance carrier | Shared (employer + stop-loss carrier) | Employer (with stop-loss protection) |

| Monthly cost structure | Fixed premium to carrier | Fixed monthly amount (claims + admin + stop-loss) | Variable: actual claims + fixed admin/stop-loss |

| Data transparency | Little to none; carrier controls data | Moderate; monthly claims reporting typical | Full visibility into every dollar spent, with the right model in place |

| Plan design flexibility | Limited to carrier’s off-the-shelf options | Moderate customization available | Complete control over plan design, with the right model in place |

| State insurance mandates | Subject to all Michigan mandates | Exempt (ERISA preemption) | Exempt (ERISA preemption) |

| State premium taxes (2 to 3%) | Yes, built into your premium | No | No |

| Carrier profit margin in cost | Yes (typically 3 to 8%) | Reduced | Eliminated |

| Surplus/refund potential | No, carrier keeps unused premium | Yes, partial refund if claims are low | Yes, all savings stay with employer |

| Best for (employee count) | Under 50 employees | 25 to 200 employees | 75+ employees |

The growth of level-funded plans has been significant. According to KFF, 37% of small firms now offer level-funded plans, up from 7% in 2019. UnitedHealthcare reports that employers who migrated to level-funded plans paid an average of 22% less than comparable fully insured premiums. Level-funding offers the budget predictability of a fully insured plan with the cost advantages of self-funding, making it an excellent entry point for employers who want to test the waters before committing fully.

Is my company ready to self-fund? A Readiness Assessment Framework

Self-funding isn’t for everyone. We’ll be the first to say that. It requires commitment, engagement, and a willingness to manage your health plan like the major business asset it is. Here are the three criteria we use when evaluating whether a Michigan employer is ready.

A. Cash Flow Stability

Self-funded plans require the ability to absorb month-to-month variability in claims. A company with consistent, predictable revenue sits in a stronger position than one with extreme seasonal swings. That said, level-funded arrangements smooth out variability with fixed monthly payments. If your business can handle a 10 to 15% variance in monthly healthcare spend without distress, you have the cash flow stability to self-fund.

B. Workforce Size and Stability

The math of self-funding works better with larger risk pools. We generally recommend at least 50 stable employees, though level-funded solutions now make it viable for groups as small as 25 in Michigan. High turnover raises concerns–not because of cost–but because it makes claims less predictable. If your annual turnover stays under 25%, you’re in good shape.

C. Risk Tolerance and Leadership Commitment

Self-funding works best when the leadership team treats the health plan as something they own, not something they hand off to a carrier. That doesn’t mean managing claims day-to-day. Your TPA handles operations. It means reviewing performance quarterly, asking the right questions, and being willing to make changes based on the data. The 2025 KFF survey found that 67% of covered workers nationally already participate in self-funded plans. This isn’t uncharted territory. Stop-loss insurance limits your downside. The real question is whether your team is ready to engage.

What does Michigan’s regulatory environment mean for self-funded plans?

This is one of the most important and most misunderstood aspects of self-funding. The regulatory framework actually favors self-funded employers, but it’s important to understand the landscape.

ERISA Preemption: Why Self-Funded Plans Hold a Regulatory Advantage

The federal Employee Retirement Income Security Act (ERISA) governs self-funded employer health plans, not state insurance law. This distinction matters. ERISA’s preemption clause exempts self-funded plans from Michigan state insurance mandates, state premium taxes (typically 2 to 3% of premium), and many state-level coverage requirements that add cost to fully insured plans. Level-funded plans also qualify for ERISA preemption because the law treats them as self-insured.

For Michigan employers operating across multiple states, this advantage compounds. Instead of navigating a patchwork of state insurance laws, your self-funded plan operates under one federal standard. The Self-Insurance Institute of America notes that Congress designed ERISA preemption specifically to prevent conflicting state regulations from driving up costs and undermining employers’ ability to offer health benefits.

What Regulations Do Self-Funded Plans Still Follow?

ERISA preemption doesn’t mean zero regulation. Self-funded plans must comply with federal requirements, including

- HIPAA privacy and portability rules

- The Affordable Care Act’s preventive care mandates

- Mental health parity requirements under MHPAEA, COBRA continuation coverage

- The No Surprises Act

- ERISA’s own reporting, disclosure, and fiduciary standards.

Your third-party administrator (TPA) handles much of this compliance on a day-to-day basis, but as the plan sponsor, you carry the fiduciary responsibility.

Michigan-Specific Considerations

DIFS doesn’t directly regulate self-funded ERISA plans, but Michigan employers should monitor several state-level dynamics.

- First, DIFS regulates Michigan’s stop-loss insurance market, so your stop-loss carrier must hold a Michigan license.

- Second, Michigan does not currently impose “attachment point” minimums on stop-loss policies (some states do), giving employers more flexibility when setting risk thresholds.

- Third, the evolving ERISA preemption debate regarding PBM regulation is relevant here in Michigan. The U.S. Supreme Court’s June 2025 decision in PCMA v. Mulready reaffirmed that states cannot force ERISA plans to adopt specific network or benefit design requirements, though states retain the ability to regulate reimbursement practices.

Michigan’s price transparency movement also deserves attention. Senate Bill 95 passed the Michigan Senate 35 to 1 and would prohibit hospitals that violate federal price transparency laws from collecting on medical debt. House Speaker Matt Hall has called for a public service commission to regulate hospital price increases. For self-funded employers, price transparency creates a real advantage.

What does the implementation timeline look like?

Transitioning from fully insured to self-funded doesn’t happen overnight, and it shouldn’t. Here’s a typical timeline for Michigan mid-market employers, working backward from a January 1 plan effective date.

Discovery and Strategy (8-12 months before effective date)

This phase begins with analyzing your current plan’s claims data (if available), benchmarking your costs against the market, assessing your workforce demographics, and building a financial model. If you’re fully insured and your carrier won’t release claims data (which happens more than you’d think), an experienced benefits advisor can work with census data and regional benchmarks to build projections. This is also the time to evaluate TPA options, stop-loss carriers, and network strategy — including whether direct contracting through a network like Nomi Health makes sense for your employees.

Plan Design and Vendor Selection (4-8 months out)

Plan structure (deductibles, copays, coinsurance, pharmacy formulary) should be designed around what the data reveals about your workforce. Your advisor will select and negotiate with a TPA, stop-loss carrier, and PBM on your behalf. For many Michigan employers, this is where the Nomi Health network comes into play: direct contracts with Trinity Health, Henry Ford, Holland Hospital, and Michigan Medicine can enable $0 deductible/$0 copay plans for in-network care, fundamentally reshaping the employee experience.

Implementation and Communication (4 months out through open enrollment)

Vendor contracts are finalized, employee communications are developed, and enrollment launches. Employee communication matters as much as plan design in this phase — your team needs to understand what’s changing and why. Plan documents (SPD) are drafted, ID cards are produced, and all systems are tested. Plan for at least 30 days of employee education before the open enrollment window opens. An experienced benefits advisor like Total Control Health Plans can manage this process end to end, ensuring nothing falls through the cracks during the transition.

What to Expect in Year One

Some clients see double-digit savings in the first year, but it’s important to remember that self-funding is a long-term strategy where cost reductions are experienced over time.

The first 90 days bring a transition period. Employees learn new processes. Your HR team gets comfortable with the TPA’s systems. The first two months in particular will see fairly few claims. However, eventually claims data begin to develop a pattern, and by month six, you’ll have enough data to start making informed decisions about plan adjustments. By month 12, you’ll hold a full year of claims data (something most fully insured employers never get), and you’ll understand exactly where your healthcare dollars go.

You won’t have to wait until year’s end to make adjustments. A huge advantage in self-funding is the ability to monitor performance in real time and make changes to avoid unpleasant surprises during renewal.

Beyond initial savings, even greater benefits may compound in later years, when you can use that data to implement targeted cost management strategies: steering to high-value providers, addressing high-cost claimants with care management, optimizing your pharmacy strategy, and negotiating better stop-loss terms with a proven track record.

What should Michigan employers do next?

The 2025–2026 renewal cycle has made one thing clear: the traditional fully insured model is not keeping up. Double-digit rate increases from DIFS, $1.7 billion in carrier losses at BCBSM, and three hospital systems controlling 64% of Michigan’s market share are not problems that resolve themselves at the next renewal. They are structural forces that will continue to drive costs higher.

Self-funding and level-funding give Michigan employers a way to respond. Not by absorbing the increases or passing them to employees, but by taking direct control of how healthcare dollars get spent. Our MI Employers Health Insurance Report found that self-funded companies rate their satisfaction with plan data 38% higher than fully insured companies. That gap in visibility translates directly into a gap in cost control. Employers who can see where the money goes can make better decisions about where it should go.

If your company has 50 or more stable employees, a manageable cash flow, and leadership willing to engage, the question is not whether self-funding can work for you. It is whether you can afford to keep doing what you’ve been doing. Contact Us for a no-obligation assessment.

Frequently Asked Questions About Self-Funded Health Plans in Michigan

These are the questions Michigan employers ask us most often. Each answer gives you a direct, actionable response.

Companies with 25 to 50 stable employees can begin with a level-funded arrangement. For full self-funding, we typically recommend at least 50 stable employees to create a sufficient risk pool with more employees often yielding more predictable savings. A company with 100 employees is well within the range where self-funding delivers consistent results. The 2025 KFF survey found that 27% of workers at firms with 10 to 199 employees already participate in self-funded plans, and 37% participate in level-funded plans. The threshold sits lower than most employers assume.

Our clients have averaged 20% savings in the first year. Industry-wide, estimates range from 8 to 15% for level-funded and 15 to 20% for fully self-funded plans. Savings come from eliminating state premium taxes (2 to 3%), removing carrier profit margins (3 to 8%), and gaining the transparency to manage costs proactively. Your actual savings depend on your current plan design, claims history, and how aggressively you pursue cost management.

Stop-loss insurance protects self-funded employers against large claims. Specific stop-loss covers individual claims exceeding a set threshold (typically $50,000 to $150,000 for mid-market employers). Aggregate stop-loss caps your total plan liability for the year. The stop-loss market reached $26.9 billion in 2024 and Allied Market Research projects it will grow to $113.5 billion by 2034. Your maximum exposure stays defined and insured.

Yes. Self-funded plans can utilize the big market players, which has both advantages and disadvantages. You can also build custom plans with independent administrators that will give you the greatest amount of transparency and flexibility. In Michigan, theNomi Health network provides direct contracts withTrinity Health,Henry Ford Health System,Holland Hospital, andUniversity of Michigan Health, often at significantly lower costs than traditional carrier-negotiated rates, with the ability to offer $0 deductible/$0 copay plans for in-network care.

ERISA is the federal law that governs employer-sponsored benefit plans. Its preemption clause means federal law regulates self-funded plans, not Michigan’s DIFS. This exempts you from state insurance mandates, state premium taxes, and state coverage requirements, all of which add cost to fully insured plans. Level-funded plans also receive ERISA preemption. You still comply with federal requirements like HIPAA, ACA preventive care mandates, and mental health parity.

A third-party administrator (TPA) handles the day-to-day operations of your self-funded plan: claims processing, network access, member services, and compliance. Yes, you need one. Selecting the right TPA ranks among the most important decisions in the transition. We evaluate TPAs based on claims accuracy, customer service, reporting capabilities, and Michigan network access.

Level-funded plans provide a fixed monthly cost (like fully insured) but deliver the regulatory and cost advantages of self-funding. Your monthly payment covers expected claims, administrative fees, and stop-loss insurance. If actual claims come in below projections, you receive a refund. Think of it as self-funding with training wheels. It’s ideal for employers who are new to alternative funding or have 25 to 200 employees. KFF data shows level-funded adoption among small firms grew from 7% to 37% between 2019 and 2025.

Plan for 8 to 12 months from the initial analysis to the plan’s effective date. The process includes data analysis and financial modeling (months 8 to 12), plan design and vendor selection (months 4 to 8), and implementation and employee communication (months 1 to 4). If you’re considering a January 1, 2027 effective date, the time to start is now.

Done well, employees should notice an improvement. Self-funded plans give you the flexibility to design benefits around what your workforce actually needs, often with lower deductibles, richer benefits, and innovative features that off-the-shelf fully insured plans can’t offer. With direct contracting through networks like Nomi Health, we’ve built plans with $0 deductibles and $0 copays that employees genuinely prefer. Clear communication during the transition makes all the difference.

Request your claims data from your current carrier (or ask your broker to request it). Even a high-level summary helps. Then talk to a benefits advisor who specializes in self-funded plan design, not your current carrier’s account rep. If you’re considering this path, reach out to our team for a no-obligation assessment that includes a financial model comparing your current plan with self-funded and level-funded alternatives.

About the Author, Mike Hill

Mike Hill is the founder of Total Control Health Plans and a 25-year veteran of the employee benefits industry. Credentialed as a Registered Health Underwriter (RHU), Registered Employee Benefits Consultant (REBC), and Licensed Insurance Consultant (LIC), Mike specializes in helping Michigan employers redesign and manage self-funded health plans that deliver real cost control and transparency.

Mike has been recognized as a BenefitsPRO Broker of the Year finalist, a Grand Rapids Business Journal 40 Under Forty honoree, and a Next Gen Benefits Mastermind Partnership Advisor of the Year. He serves on the Ault International Medical Management (AIMM) Agent Advisory Council and is a regular speaker at national industry conferences including the World Healthcare Congress and BenefitsPRO Broker Expo. He is also the author of Not Rocket Surgery: An Employer’s Guide to Controlling the Health Care Supply Chain.

Mike founded Total Control Health Plans in 2018 with a straightforward belief: employers deserve the same insight, performance, and control over their health insurance as they would expect from any other supplier. He and his team work exclusively with closely-held and midmarket Michigan businesses ready to stop absorbing cost increases and start managing their health plan like the business asset it is.

Sources

Mercer, 2025 National Survey of Employer-Sponsored Health Plans (November 2025)

KFF, 2025 Employer Health Benefits Survey (October 2025)

Michigan DIFS, 2026 Approved Rate Changes (michigan.gov)

SHADAC/MEPS-IC, Employer-Sponsored Insurance Cost Analysis, Michigan (January 2026)

PwC Health Research Institute, Medical Cost Trend: Behind the Numbers 2026 (July 2025)

Aon, U.S. Employer Health Care Costs Expected to Rise 9.5% in 2026 (2025)

Segal, 2026 Health Plan Cost Trend Survey (September 2025)

Business Group on Health, 2026 Employer Health Care Strategy Survey (2025)

Crain’s Detroit Business, Michigan Blue Cross Reports $1B Loss for 2024 (2025)

Bridge Michigan, Michigan Open Enrollment: How Much Rates Are Rising (October 2025)

PCMA v. Mulready, 10th Circuit / U.S. Supreme Court (June 2025)

Allied Market Research, Stop Loss Insurance Market Size (2024)

Total Control Health Plans, MI Employers Health Insurance Report (2025)

American Medical Association, Competition in Health Insurance: A Comprehensive Study of U.S. Markets (December 2024 data, published December 2025)