There are three major developments that are starting to crack the traditional PBM model. Continue reading this article to learn what they likely mean for your pharmacy spend over the next few years.

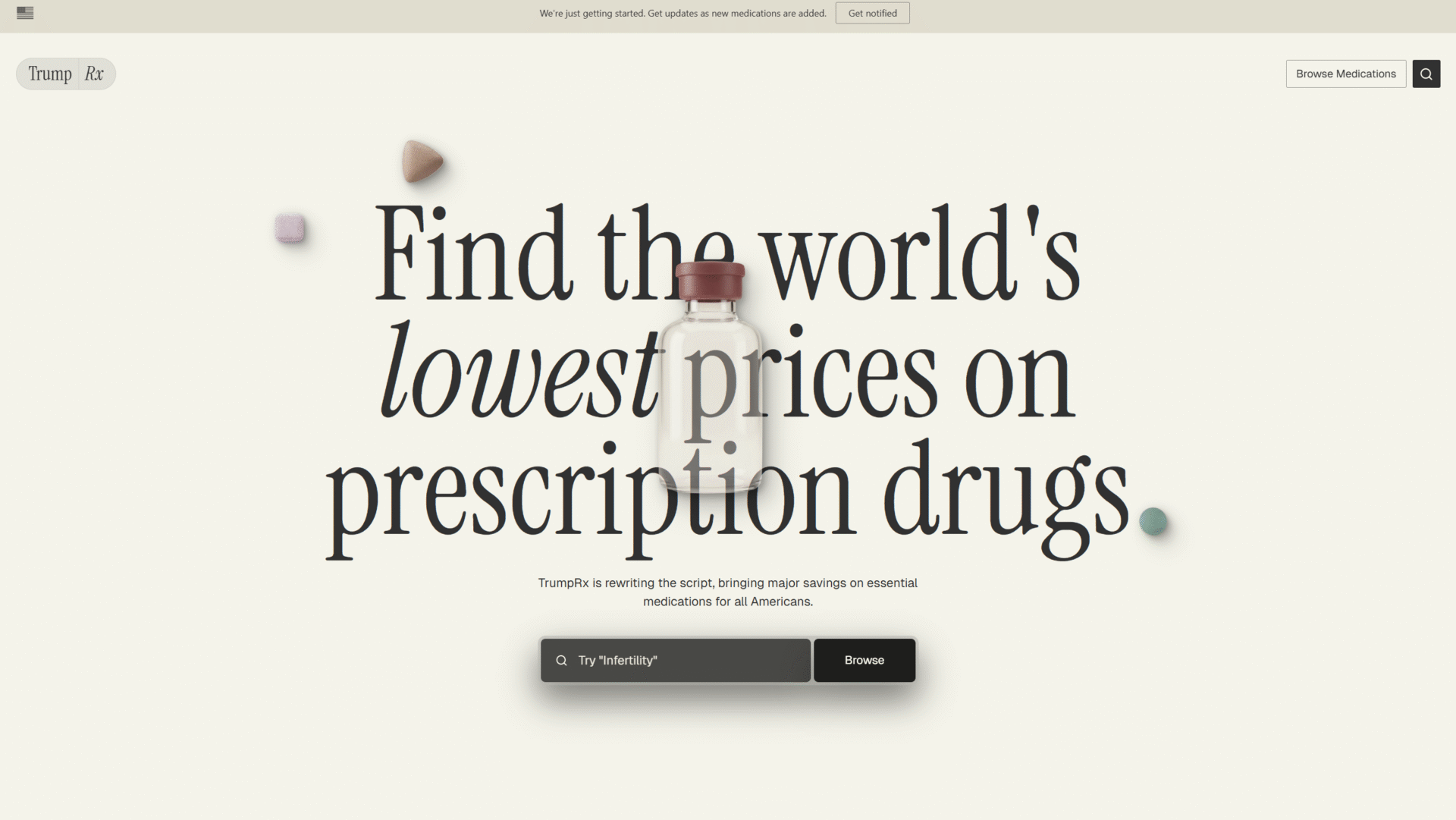

Development 1. TrumpRx.gov – Public Price Transparency

The launch of TrumpRx.gov on Thursday, February 5th is a big step toward making prescription drug pricing visible to everyone, not just PBMs and carriers. It’s designed to:

- Publish benchmark pricing and discounts for a wide range of drugs.

- Make it easier for employers, consultants, and consumers to see when “negotiated” prices don’t match the purported discounts.

What it Means for You

Over time, it becomes much harder for PBMs to hide spread pricing and opaque rebate practices when reference prices are just a few clicks away. Expect more leverage in negotiations, more pressure to justify “admin fees,” and an easier path to compare transparent pass through models against traditional contracts. In the immediate term we are working to find the most cost effective way for employers to leverage GLP-1 pricing through this platform if they’d like to provide access to these medications for weight loss purposes.

In the immediate term, TrumpRx.gov appears to be the most cost effective option for consumers to get these brand name medications, especially as the FDA is taking steps to crack down on distributors of compounded GLP-1 medications like the online pharmacy Hims/Hers.

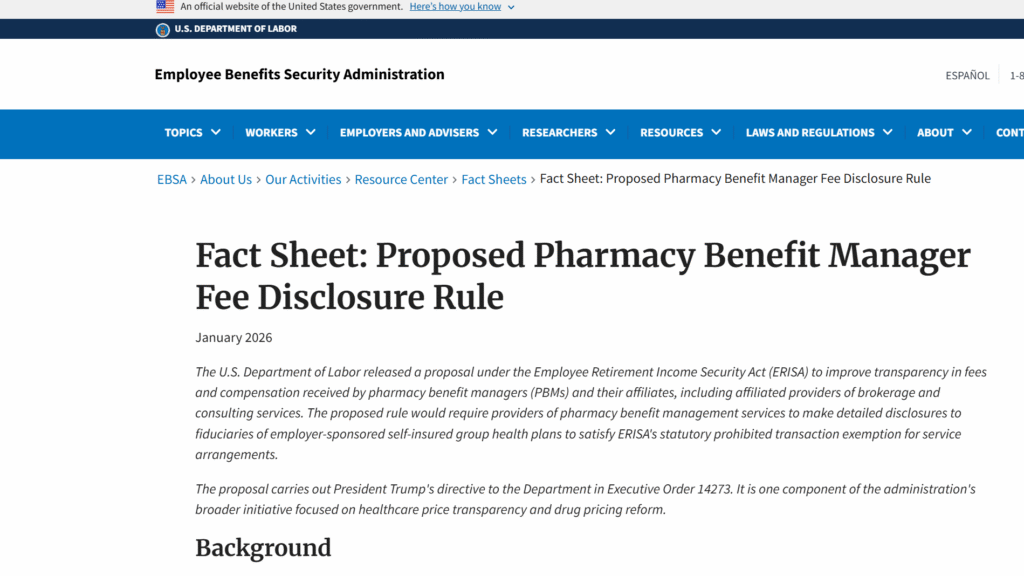

Development 2. Proposed DOL PBM Transparency Rules and Timing

The Department of Labor’s proposed PBM transparency rules, which were released on January 30th, would treat PBMs as covered service providers to ERISA health plans, requiring detailed disclosure of:

- All forms of direct and indirect compensation (rebates, fees, spreads, admin charges, pharmacy clawbacks).

- Contractual terms that affect pricing, spread, and rebate retention.

- Audit rights for plan fiduciaries, and a path for fiduciaries to notify DOL when PBMs don’t cooperate.

The proposed rules are expected to be finalized in the near term (likely for plan years beginning in 2027 or 2028, depending on the final rule and transition periods), with some obligations potentially applying earlier on a prospective basis once finalized. Unlike many rules from the government which are often watered down with little teeth, these rules were written by someone who knows what they are doing. This will have a massive impact on transparency, and will likely also contribute to costs coming down. Additionally, it appears these rules will be “politics proof” meaning neither side of the aisle will want to take the lead on eliminating them once they go into effect.

What it Means for You

- Give you a formal right and process to demand PBM compensation transparency.

- Increase the fiduciary expectation that employers review PBM compensation as a prohibited transaction and reasonableness issue, not just a vendor invoice.

- Make it easier to move away from opaque spread pricing models toward pass through and/or fee based arrangements.

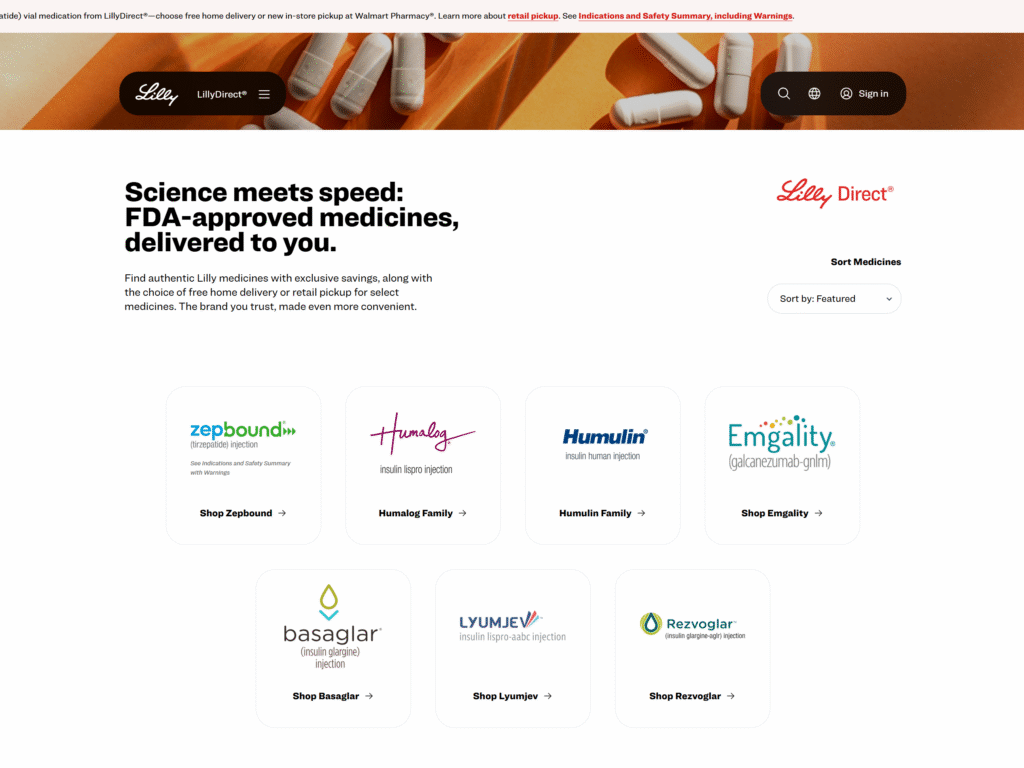

Development 3. Direct-to-Employer Pricing from Eli Lilly & Novo Nordisk

Two of the most important players in today’s pharmacy trend—Eli Lilly and Novo Nordisk—have now stood up direct programs to employers and plans for high cost medications, especially GLP 1s for diabetes and obesity.

These programs typically:

- Offer direct contracts with employers or plan sponsors (sometimes through TPAs or coalitions) at a clearer net price.

- Reduce or bypass traditional PBM spread and some rebate complexity.

- Create a template other manufacturers can follow for high impact therapeutic classes.

What it Means for You

The initial direct to employer options focus solely on GLP-1 medications and frankly the pricing isn’t very compelling, however, this could be the tip of the iceberg in sidestepping pharmacy benefit managers which could be a very big step. Over the next few years, we’re likely to see:

- More carve outs for specific therapeutic classes (GLP 1s, specialty injectables, etc.).

- Direct, volume based agreements where the plan’s net price and guarantees are much clearer.

- Increased pressure on PBMs to either match these net prices or risk losing those classes altogether.

What this Signals About the Future of Rx Pricing

Taken together, these three developments point in the same direction:

- Less opacity, more direct contracting. Public benchmarks, manufacturer direct programs, and formal PBM disclosure rules all push the market toward clearer unit prices and away from “we’ll make it up on rebates.”

- Pressure on traditional PBM margins. As spread and hidden compensation become harder to sustain, PBMs will either shift to more transparent admin fee models or risk losing high value categories to direct arrangements.

- More leverage—and more responsibility—for employers. You will have better tools and more leverage to challenge current contracts, but also a stronger fiduciary expectation to use that information (review compensation, run RFPs, consider alternative models, and document decisions).

What You Can Do Now

Over the next 12–24 months, the most proactive employers will:

• Ask current PBMs for full compensation disclosure and audit rights in renewals.

• Model direct or carved out arrangements for key drug classes like GLP 1s, factoring in clinical management and member experience.

• Align with TPAs, coalitions, or transparent PBMs that are already built around pass through pricing and clear admin fees.

If you’d like a short call to walk through what this means for your plan specifically, let’s connect.